Knight-Swift Transportation believes the worst of the freight cycle has passed. It is seeing some benefit from its decision to trim the truckload fleet as asset utilization is improving. It said it will continue to allocate capital to the expansion of its less-than-truckload business through both organic growth and acquisitions.

“We don’t want to be too quick to call it but I think we’re cautiously optimistic that certainly the trough is behind us and we’re on our way to building back,” CEO Adam Miller told analysts on a Wednesday evening call.

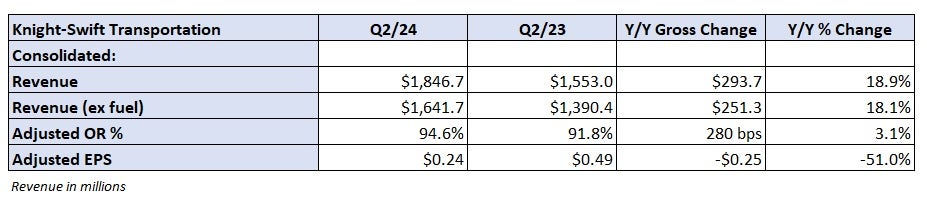

Knight-Swift (NYSE: KNX) reported adjusted earnings per share of 24 cents for the second quarter, which was 3 cents below the consensus estimate and below management’s guide of 26 to 30 cents. The largest exclusions from the adjusted result were tied to acquisition-related costs and noncash impairments on equipment and real estate.

The result included a 6-cent hit, or $12.5 million, due to the settlement of an auto liability claim. Lower gains on equipment sales were a 4-cent headwind compared to the year-ago quarter (assuming a normalized tax rate). Higher interest expense and a higher tax rate were a 10-cent y/y headwind.

The company maintained adjusted EPS guidance of 31 to 35 cents for the third quarter, which compared to the consensus estimate of 34 cents at the time of the Wednesday print. It issued fourth-quarter guidance of 32 to 36 cents, which was lower than the 45-cent consensus estimate. The company’s earnings outlook assumes no material change in market conditions and includes the negative impact from a higher effective tax rate for the remainder of the year.

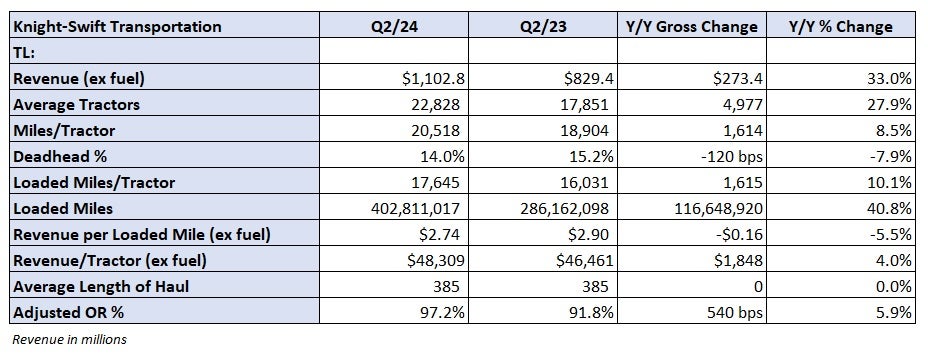

Truckload revenue increased 33% year over year to $1.1 billion due to the acquisition of U.S. Xpress on July 1, 2023. Excluding the acquisition, the unit’s revenue was 6% lower y/y.

Average tractors in service increased 28% y/y with revenue per tractor up 4% excluding fuel surcharges. The increase in revenue per tractor was the result of a 9% increase in miles per tractor, which was partially offset by a 6% decline in revenue per loaded mile (excluding fuel). The company has been focused on improving asset utilization throughout the downturn, culling excess equipment, primarily trailers.

Management said fundamentals continue to firm and that spot freight and unplanned loads are no longer getting discounts.

The TL unit recorded a 97.2% adjusted operating ratio (operating expenses expressed as a percentage of revenue), which was 540 basis points worse y/y. The accident claim was a 120-bp headwind to the OR while U.S. Xpress’ operations, which were again breakeven during the quarter, were a 130-bp drag.

The company’s EPS guidance assumes slight sequential improvement in TL revenue in both the third and fourth quarters, with the adjusted OR improving to the low- to mid-90% range. Knight-Swift has reconstructed U.S. Xpress’ business, which was heavily tied to the spot market at the time it was acquired. The unit is now seeing double-digit price increases as it closes the rate gap to Knight-Swift’s legacy operations.

Knight-Swift has acquired or assumed leases on 56 LTL terminals since entering the LTL market three years ago. It opened 11 LTL terminals in the second quarter after opening seven in the first quarter. It plans to open another 20 by the end of the year, giving it a 22% increase to door count in 2024 alone.

The additions come as the company continues to fill in the gaps of what will become a national network. Management said it would be disappointed if it couldn’t complete an LTL acquisition within the next 12 months.

The LTL unit reported a 15% y/y increase in revenue to $263 million during the quarter as both shipments and revenue per shipment (excluding fuel) increased by 8%. Revenue per hundredweight, or yield, was up 13% y/y excluding fuel. The yield calculation partially benefitted from a 5% y/y decline in weight per shipment. The unit recorded an 85.9% adjusted OR, which was 80 bps worse y/y.

Guidance calls for the unit to see low double-digit y/y revenue increases the rest of the year with shipments up by a mid-single-digit percentage and yield improving by high-single digits. The unit’s OR is expected to be in the mid- to high-80% range as costs associated with opening new locations present a drag on margins.

The logistics business, which includes truck brokerage, saw revenue improve 12% y/y to $132 million. The freight mix at U.S. Xpress was credited with pushing revenue per load 11% higher y/y as volumes were up just slightly. The segment recorded a 95.5% adjusted OR, 390 bps worse y/y but 160 bps better than in the first quarter.

Knight-Swift’s intermodal unit booked a fifth consecutive operating loss in the quarter.

Shares of KNX were off 0.7% in after-hours trading on Wednesday.